Risk Tolerance vs. Risk Capacity

Kudos to Michael Kitces for another informative research article on the important differences between investment risk tolerance and financial risk capacity. In this blog post, I’ll add to risk assessment discussion by introducing an alternative method for measuring financial risk capacity.

In general terms, risk tolerance or risk preference is your emotional willingness to accept more investment risk for an expected higher return. Risk capacity, on the other hand, is essentially your ability to live with the outcome of depending on risky assets to build a sufficient retirement nest egg. The previous statement is my opinion of what risk capacity really is. The more classic definition is how much risk a client can afford to take without risking his/her objectives.

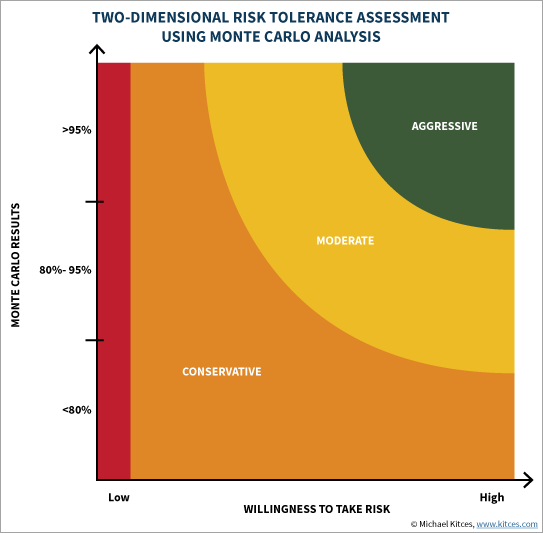

In the Kitces article, Michael points out the importance of measuring both types of risk separately in order to prevent the averaging of the two measures leading to inaccurate client risk profiles. He further demonstrates how Monte Carlo financial scenario planning provides a good measure of risk capacity and can be helpful when combined with traditional risk preference analysis.

Source: Michael Kitces, www.kitces.com

Rather than depend on Monte Carlo probabilities of success, I’m suggesting that funded ratio, current household assets divided by future living expenses, is a better measure of risk capacity and should be favored in two-dimensional assessment of financial risk.

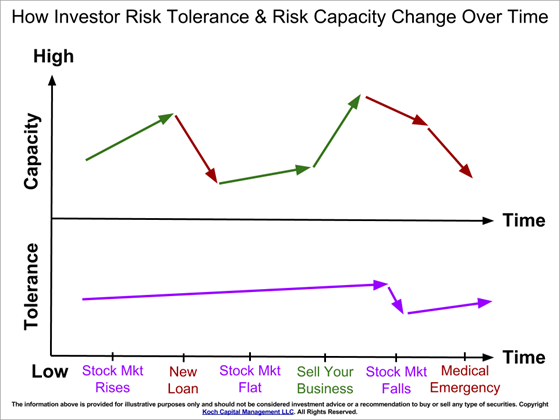

Risk Capacity Changes Over Time

Traditional risk tolerance tends remain relatively stable over an investor’s lifetime. That is until the investor experiences a huge portfolio drawdown like in 2008-09, then preferences always get more conservative much to the consternation of most advisors who recognize that the time to load up on stocks is when the public is terrified of the market.

Source:Koch Capital

Rick capacity can fluctuate considerably over an investor’s lifespan for the simple reason that it includes non-investment life events that affect a household’s financial capability to accept risk. Life happens. And even the best portfolio returns may not be enough to counter the negative financial effects of an unplanned medical emergency or personal crisis.

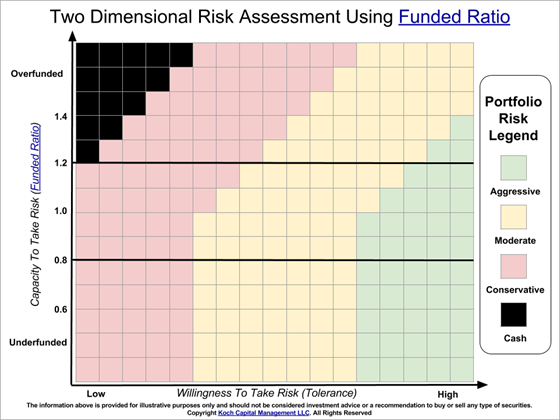

When using the funded ratio approach to measure household risk capacity, you’re not only accounting for both investment and non-investment assets, but also using a measurement system that can be updated daily to help you quickly adapt your investment plan before your lifestyle is impacted. At Koch Capital, we think of household funded ratio monitoring as a real-time compass to help guide you to and through retirement.

Source:Koch Capital

When using the funded ratio as your household’s risk capacity measure, you are essentially accounting for all the household asset resources at your disposal. These assets include your current financial accounts like IRAs and 401ks, your real property holdings, your future ability save money, and your future pension and social security benefits.

In academic parlance, these three reservoirs of savings are referred to as: Financial Capital, Human Capital, and Social Capital. Since risk tolerance (preference) tends to focus on just the Financial Capital side of the equation, you need a mechanism to map the investor’s risk tolerance back to the broader household’s financial risk capacity.

At Koch Capital, we use Riskalyze to measure client investment risk preference; specifically how much portfolio loss an investor can tolerant before he or she hits the eject button. On the risk capacity side, we use our own proprietary funded ratio tool to measure the household’s capacity to accept risk, right up to the dollar amount where the client’s lifestyle is impacted. The diagram below demonstrates how the two measures intersect in the two-dimensional risk assessment framework.

Source:Koch Capital

In this two-dimensional risk assessment framework, risk capacity (funded ratio) influences risk tolerance more than tolerance affects capacity. This is because an investor’s risk tolerance, for example, to be aggressively invested on the Financial Capital (portfolio) side is also influenced by the household’s other risk capacity resources—Human Capital and Social Capital.

For example, if your funded ratio (household assets dividend by future liabilities) is over 1.0 and your conservative Social Security benefits constituents the largest portion of your Financial, Human and Social Capital mix, then your retirement plan can probably withstand a more aggressive portfolio allocation on the smaller Financial Capital portion of your overall household asset base.

Stress Test Your Lifestyle Resilience Before Investing Capital

Let’s look at a numerical example of mapping your risk tolerance (Riskalyze) number into your risk capacity (funded ratio) using the two-dimensional risk assessment framework. First, you need to calculate your risk tolerance for all your household’s investment portfolios. I referred to this previously as your Financial Capital.

Source:Koch Capital, Riskalyze

Ideally, the retirement-aspiring investor should obtain a single, aggregated Riskalyze number for all portfolios associated with the household. One way to approximate this aggregated value is to (1) calculate/estimate a Riskalyze number for each investment account using the free Riskalyze risk assessment service, then (2) create a spreadsheet to calculate the weighted average Riskalyze number, or 57 in my educational example above.

Next, derive your potential portfolio loss number by using the following Riskalyze hack. Create a dummy Riskalyze client and enter your weighted average risk number and the total value of your investment accounts. In my example, the weighted average, target risk level is 57 and the aggregate account balance is $3,353,106.

Riskalyze provides both the potential downside loss and upside gain over the subsequent six months (see below). Unfortunately, either you or your advisor or your advisor friend will need to be registered Riskalyze user to gain access to this hack.

Source: Riskalyze.com

For this example, the -11% potential loss percent or -$384,870 potential loss number is what I’m looking for as a numerical expression of the client’s aversion to investment losses. Please remember that it’s just a downside estimate and by no means 100% accurate, but still a useful estimate to map against the investor’s risk capacity. The estimated downside loss number will tell us if the investor’s risk tolerance matches up with the reality of the household’s current financial capacity to accept this level of investment risk.

For the statistical inclined, the resulting downside loss number is a two standard deviation forecast over the next sixth months of how much this combination of portfolios could lose (or gain) without you hitting the panic button. But just know that a true black swan event, though rare, would result in a three or more standard deviation loss, and possible permanent loss of capital if the investor sells near the bottom and/or the subsequent market recovery doesn’t materialize. Hence, we are stress testing for the less severe, but more likely market correction scenario.

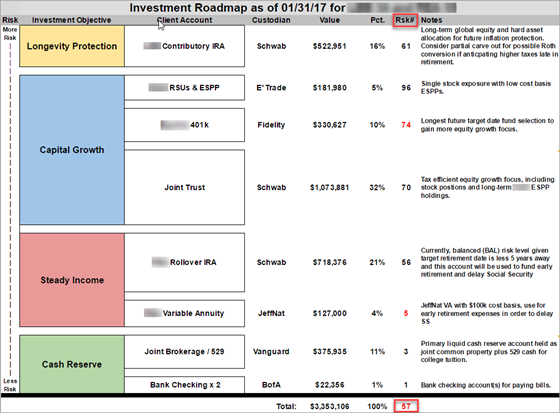

Now let’s switch over to the risk capacity side using Koch Capital’s risk capacity tool.

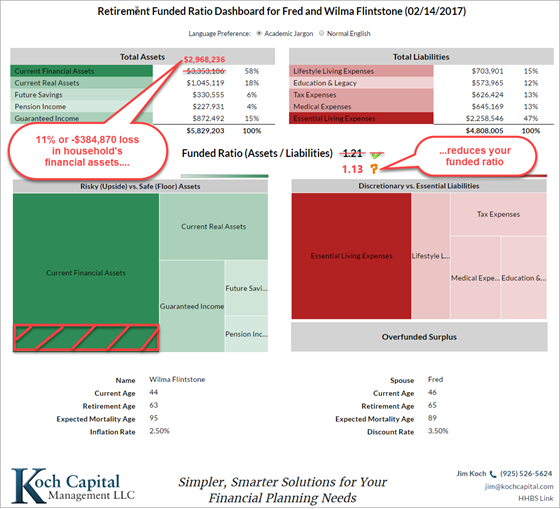

Click here for balance sheet image field descriptions

Source: Koch Capital

The graphic above is an annotated screenshot example of Koch Capital’s dashboard app which calculates the household’s current funded ratio. It shows that 11% drop in this household’s portfolios translate to a reduction in its funded ratio from 1.21 (overfunded) to 1.13 (constrained). While this potential portfolio drop would be emotionally troubling, it’s not enough to change the retirement funding trajectory in this example since the funded ratio is still greater than one and the target retirement date is still many years away.

This example also demonstrates why shifting funds from your more risky investment assets to your safer income assets (government bond ladders, annuities, etc.) will limit the downward funded ratio pressure. The riskier investment side of household asset pie would become smaller, thus less of a potential negative influence on household’s funded ratio. This risk reduction strategy is referred to as the “safety-first” approach to retirement income planning.

Beans and Rice, Rice and Beans

As debt-free maven Dave Ramsey frequently points out, “you have to live like nobody else, to live like nobody else.” And if that takes an inexpensive diet of rice and beans for a while to help pay off an expensive credit card balance, then you control your personal finance destiny, even on a modest income.

I bring this up for the simple reason that I have devoted way too much attention to Financial Capital, investment risk and growing your nest egg through stock market investing. In reality your Human Capital (ability to earn income and save) is usually your best wealth generation asset. And in most cases, it’s less risky than depending on stock market gains.

As Dave points out, “change starts with you.” Even the best investment managers cannot predict what the stock market will do next. But you control your ability to save for specific financial goals.

The funded ratio planning approach helps you intelligently budget for the future known goals (home, college, retirement, legacy, etc.) and plan for future unknown costs (medical emergency, family crisis, etc.), then guides you down the path to the lifestyle you desire and can afford.

Your greatest household asset is your ability to earn income and save for the future. And whether you are saving for a house or saving for retirement, you probably have more risk capacity than you think.

Thank you for your interest and appreciate your feedback......Jim

Household Balance Sheet and HHBS are a registered service marks of the Retirement Income Industry Association (RIIA)

Additional Resource Links

Michael Kitces - Adopting A Two-Dimensional Risk Tolerance Assessment Process:

Moshe Milevsky - It’s Time to Retire Ruin (Probabilities):

Riskalzye Blog - And the Average Risk Number is….

Jim Koch - Should You Be 100% Invested In Stocks?

Jim Koch - Retirement Funded Ratio: The One Number Every Retirement Seeking Investor Should Know And Manage:

About Jim Koch

Jim Koch is the Founder and Principal of Koch Capital Management, an independent Registered Investment Advisor (RIA) in the San Francisco Bay Area. He specializes in providing customized financial solutions to individuals, families, trusts, business entities and other advisers so they are better able to achieve their goals. Jim sees himself as an “implementer” of financial innovation, using state-of-the-art technology to provide practical investment management and retirement planning solutions for clients.

General Disclosures

This information is provided for informational/educational purposes only. The opinions referenced are as of the date of publication and are subject to change due to changes in the market or economic conditions. Nothing presented herein is or is intended to constitute advice to use or buy any of third-party applications presented here, and no purchase decision should be made based on any information provided herein. The information contained herein, while not guaranteed as to the accuracy or completeness, has been obtained from sources we believe to be reliable.

Third Party Information

While Koch Capital has used reasonable efforts to obtain information from reliable sources, we make no representations or warranties as to the accuracy, reliability, timeliness, or completeness of third party information presented herein. Any third party trademarks appearing herein are the property of their respective owners. At certain places on this website, live 'links' to other Internet addresses can be accessed. Koch Capital does not endorse, approve, certify, or control the content of such websites, and does not guarantee or assume responsibility for the accuracy or completeness of information located on such websites. Any links to other sites are not intended as referrals or endorsements, but are merely provided for convenience and informational purposes. Use of any information obtained from such addresses is voluntary, and reliance on it should only be undertaken after an independent review of its accuracy, completeness, efficacy, and timeliness.

No comments:

Post a Comment

Note: Only a member of this blog may post a comment.