Heck of a Bull Run in Bonds

If you have been following the bond market pundits like Bill Gross, Gary Shilling, Jeffrey Gundlach and others, it will come as no surprise that the 10-year U.S. Treasury bond yield recently dipped below 1.4% for the first time ever. And when you consider that foreign 10-year government bonds from Germany, Japan and Switzerland are generating negative yields, we’re definitely in uncharted bond waters both here and overseas.

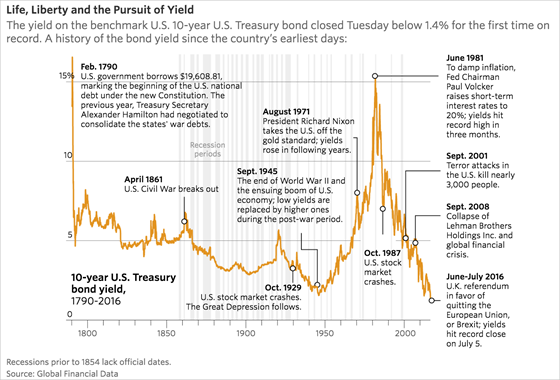

Given that bond prices move inversely to bond yields, one can see from the chart below the amazing 35-year tailwind that Treasury bonds have enjoyed to date. Now with bond prices at all time highs and bond yields at record lows, what should investors do with this traditional stable asset class?

Given that bond prices move inversely to bond yields, one can see from the chart below the amazing 35-year tailwind that Treasury bonds have enjoyed to date. Now with bond prices at all time highs and bond yields at record lows, what should investors do with this traditional stable asset class?

Source: Wall Street Journal

In general, bond investors evaluate the following five levers to target expected yield and manage risk within the fixed income portion of their investment portfolios: quality (credit risk), liquidity, maturity/duration (sensitivity to interest rates), purchasing power (sensitivity to inflation), and asset location (taxes). For this example, let’s assume the bond portfolio resides in a tax-deferred account like an IRA, so the asset location is set and bond interest received within the account is not taxed. Further, let’s assume all bonds discussed in this post are high quality, investment-grade or better, to remove the credit risk lever from consideration. So now let’s think about your bond holdings just in terms of trading liquidity, interest rates and inflation sensitivity.

Do You Really Need Bonds in Your Portfolio?

Some advisors don’t hold any bonds within their client portfolios, instead relying on third-party guaranteed income streams like insurance annuities, corporate defined benefit pensions, bank certificates of deposit and social security to fill the traditional fixed income role. In addition, this school of thought may recommend that a client hold two years of living expenses in cash to avoid portfolio distributions (sequence risk) during a severe stock market downturn like in 2008-2009.

While the “hold no bonds” strategy partially deals with the inflation sensitivity issue (with CPI-adjusted Social Security benefits and possibly inflation-adjusted annuities) and with interest rate sensitivity (income lasts for your exact lifetime), the liquidity (locked in except for cash and CDs), legacy and product cost issues are major hurdles when pursuing the bond alternative route.

The more traditional fixed income approach is to hold some taxable bonds in your IRA to help control overall portfolio risk. But if your bond holdings, with the recent record high bond prices and low yields, are now a potentially risky asset, how can you get that fixed income stability back into your investment portfolio?

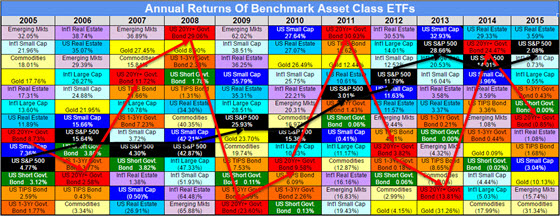

To see the traditional relationship between the stocks and bonds, please review my periodic table of benchmark ETF returns below. In particular, please note how the long-term Treasury bond (red) tends to go up in years when the S&P 500 stock index (black) goes down. This is considered normal non-correlated asset behavior at least for the past ten years. However, the period were in now is anything but normal.

Click here to view a full screen version of this graphic

Source: Koch Capital

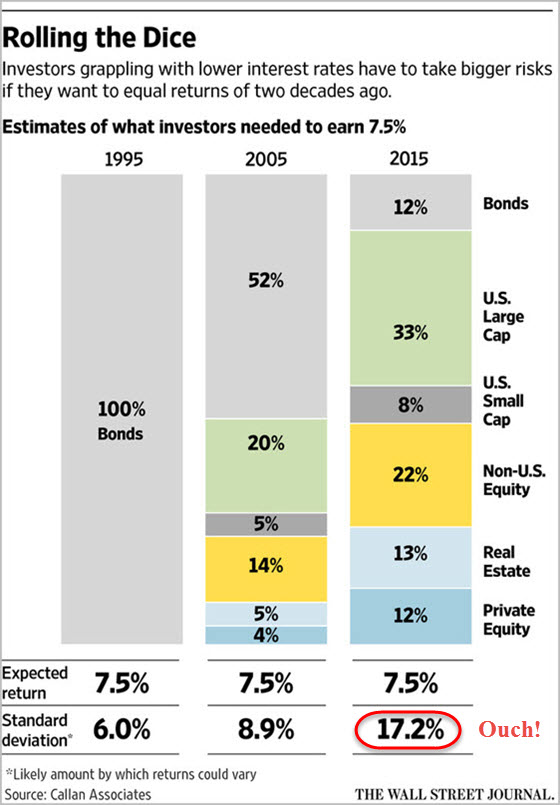

Interestingly, the big pension plans like the California Public Employees’ Retirement System (Calpers) have taken notice of this generational-long decline in bond yields and have had to ratchet up their equity allocations in order to achieve a reasonable rate of return to meet their future pension payout liabilities. Households planning for retirement have had to do this too; increase their equity allocations to augment their periodic savings in order to build a sufficient retirement nest egg. In the Wall Street Journal example below, pension funds used to simply invest in high-grade corporate bonds to achieve a reasonable 7.5% rate of return with low volatility (standard deviation) of 6.0%.

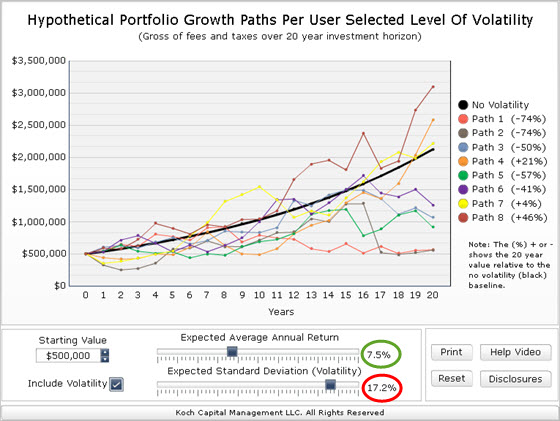

As of 2015, the bond allocation averages have declined from 100% to just 12% of the overall portfolio allocation in order to maintain that target 7.5% nominal return. However, holding more equities increases portfolio volatility (17.2% versus 6.0%) as well as the potential risk of not meeting their funding needs. To visualize what the potential roller coaster ride of 7.5% returns with 17.2% volatility looks like, please see my volatility of returns visualizer below. Yippee ki yay!

Click here to view a full screen version of this flash-based application

Source: Koch Capital

Do What the Hedge Funds and Bond Fund Managers Do

If overall portfolio growth and stability, rather than just income generation, are your primary investment goals, then consider hedging your bond holdings to be less interest rate sensitive, more inflation friendly, and easily liquidated if cash is needed. The descriptive table below contains investment metrics for the iShares Core US Aggregate Bond ETF (AGG), a common proxy for the US bond market, and my custom bond ETF mix from Koch Capital’s Global Risk-Managed Flexible Core (FLEX) portfolio strategy, available on Charles Schwab’s Managed Accounts platform.

Description

|

Size

|

Cor.

|

E.R.

|

E(Ret)

|

E(Vol)

|

Beta

|

Yield

|

AGG Bond ETF

|

38.77B

|

-2%

|

0.09%

|

2.13%

|

3.64%

|

-1%

|

2.31%

|

FLEX Bond Mix

|

0.796B

|

13%

|

0.15%

|

2.51%

|

2.87%

|

10%

|

1.59%

|

Disclosure: (1) Size is net asset value of the fund or ETF as of 7/11/2016; (2) Cor. is the 2yr historical correlation with SPY as of 7/11/2016; (3) E.R. is the fund’s expense ratio or internal management fee; (4) E(Ret) is the forecasted future annual rate of return from 7/11/2016; (5) E(Vol) is the forecasted future standard deviation from 7/11/2016; (6) Beta is the 2yr historical beta as of 7/11/2016; (7) Yield is the trailing 12 month yield as of 7/11/2016; (8) The average net asset value of multiple ETFs as of 7/11/2016. Source: Koch Capital, Quantext Portfolio Planner, Yahoo Finance

Please remember that all these measures will change depending on the time period selected.

A quick review of the table above demonstrate that both bond solutions retain their low correlations with stocks via the low or negative (Cor)elation numbers as well as low stock market Beta numbers. Both have relatively low yields at 2.31% and 1.59% respectively, but that’s to be expected in a low yield environment where we want to maintain high credit quality and not chase higher yields in the junk bond market.

Interestingly, the long-term expected return and expected volatility (standard deviation) of the FLEX bond mix is better than AGG’s. However, this is a forward-looking forecast, so who knows whether it will materialize or not. Finally, the expense ratios for both bond solutions are cheap at 0.09% and 0.15% respectively. Hard to imagine this type of high quality, low-cost bond solution available ten or even five years ago!

Now, let’s take our single AGG ETF and FLEX bond mix and run them through various macroeconomic scenarios to see how they react to specific market and economic factors.

Market & Economic Stress Tests

If Scenario Below Occurs, Then……..

|

AGG Bond ETF

|

FLEX Bond Mix

|

S&P 500 Recession, Market Down by 20%

|

4.91%

|

1.30%

|

S&P 500 Recovery, Market Up by 20%

|

-6.83%

|

-1.11%

|

Short-Term Rates Up (12M T-Bill @ 2%)

|

-8.00%

|

-3.65%

|

Long-Term Rates Up (10Yr Treasury @ 3%)

|

-7.32%

|

-3.08%

|

General Inflation Up (CPI @ 3%)

|

-3.77%

|

0.54%

|

Source: Koch Capital, HiddenLevers

Again, all these measures will change depending on the time period selected, so please focus on the directional trend rather than the absolute value, which is also subject to modelling error.

In the case of a significant 20% stock market correction, AGG will most likely perform its traditional portfolio stabilizer role of providing some positive price appreciation relief in an otherwise negative stock return swoon. The FLEX bond mix will probably return some positive price appreciation too, just not as much as the AGG for the bond portion of your portfolio.

However, the FLEX portfolio strategy is more concerned about potential bond return drag if interest rates and/or inflation creeps up, or the stock market melts up by 20% in which case the hedged FLEX bond mix will probably perform better by losing less than AGG. Even though the current low interest rates may remain low for an extended period or the current low inflation environment remains benign longer than anticipated, it’s still more painful from a long-term portfolio sustainable growth perspective to be on the wrong side of rising rates and inflation if you are investing for retirement. But that’s just one financial advisor’s opinion.

Hey, Do You Have an ETF For That?

The good news is that we are living in golden age of fund innovation where specialized financial tools can be implemented in your portfolios at reasonable cost to help protect against specific bad outcomes associated with unpredictable markets and economic conditions. However, all investment strategies come with trade-offs, usually giving up some return potential now to protect against some really bad future condition later. But with proper hedging of your bond portfolio, you can choose to dial back your stock market risk by increasing your bond allocation if you prefer a less bumpy, but slower growth ride.

In summary, all investors can now start thinking more like a hedge fund or bond fund manager, and implement their own custom hedging strategies to help protect against the market and economic conditions that most impact their chances of a secure, lifelong retirement. Like with tennis, it’s the player who is best prepared and makes fewest unforced errors that wins the match. Call me at 925-838-2324 if you like to discuss your potential bond-aggedon.

Thank you for your interest........Jim

About Jim Koch

Jim Koch is the Founder and Principal of Koch Capital Management, an independent Registered Investment Advisor (RIA) in the San Francisco Bay Area. He specializes in providing customized financial solutions to advisors, individuals, families, trusts and business entities so they are better able to achieve their goals. Jim sees himself as an "implementer" of financial innovation, using state-of-the-art technology to provide practical investment management and retirement income planning solutions for clients.

General Disclosures

This information is provided for informational/educational purposes only. The opinions referenced are as of the date of publication and are subject to change due to changes in the market or economic conditions and may not necessarily come to pass. Nothing presented herein is or is intended to constitute investment advice, and no investment decision should be made based on any information provided herein. The information contained herein, while not guaranteed as to the accuracy or completeness, has been obtained from sources we believe to be reliable. Past performance is no guarantee of future results.

Any forward looking statements or forecasts are based on assumptions and actual results are expected to vary from any such statements or forecasts. No reliance should be placed on any such statements or forecasts when making any investment decision. Under no circumstances does the information contained within represent a recommendation to buy or sell any particular security or pursue any investment strategy. There is a risk of loss from an investment in securities. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment will be profitable or suitable for a particular investor’s financial situation or risk tolerance. Please refer to the Site Disclosure page for additional information.

Nothing contained herein should be interpreted as legal, accounting, or tax advice. Any tax statements contained herein were not intended or written to be used, and cannot be used for the purpose of avoiding U.S. federal, state or local tax penalties. Tax issues can be complicated. Please consult your tax advisor for personal tax questions and concerns.

Use of Calculators, Planning Tools, and Other Devices

The use of any calculator, tool, or similar device contained within or linked to this website is subject to your acknowledgement and understanding that the projections or other information generated by any such tools is not, and should not be construed, in any manner whatsoever, as the receipt of, or a substitute for, personalized individual advice from Koch Capital, or from any other investment professional. The projections or other information generated by such tools regarding the likelihood of various investment outcomes are hypothetical in nature, do not reflect actual investment results, are not guarantees of future results, and may not reflect the actual growth or costs of your own investments. These tools are designed for informational and educational purposes only and should not be considered investment advice. No reliance should be placed on any such information when making an investment decision. Koch Capital makes no warranties of any kind, and disclaims liability to any person for any actions taken or omitted in good faith with respect to such tools. Koch Capital obtains the information provided via these tools from third party sources believed to be reliable but not guaranteed. Koch Capital is not responsible for the consequences of any decisions or actions taken as a result of information provided by such tools and does not warrant or guarantee the accuracy or completeness of the information requested or displayed. Please refer to the Site Disclosure page for additional information.

Third Party Information

While Koch Capital has used reasonable efforts to obtain information from reliable sources, we make no representations or warranties as to the accuracy, reliability, timeliness, or completeness of third party information presented herein. Any third party trademarks appearing herein are the property of their respective owners. At certain places on this website, live 'links' to other Internet addresses can be accessed. Koch Capital does not endorse, approve, certify, or control the content of such websites, and does not guarantee or assume responsibility for the accuracy or completeness of information located on such websites. Any links to other sites are not intended as referrals or endorsements, but are merely provided for convenience and informational purposes. Use of any information obtained from such addresses is voluntary, and reliance on it should only be undertaken after an independent review of its accuracy, completeness, efficacy, and timeliness.

No comments:

Post a Comment

Note: Only a member of this blog may post a comment.